The True Math of Renting vs. Buying A Home

A Breakeven Financial Model To Help Weigh The Trade Offs Of Property Ownership.

The decision to rent or buy a home is a significant one. Everyone has a vocal opinion, including your parents and extended family, who may have outdated views on home ownership equating to financial stability and success. In some cities such as New York, renters make up nearly 70% of all residents in the city. There must be some logic behind all these Millionaires continuing to rent.

Let’s take all the emotional elements of this decision and throw them out the window. We are just going to stick with the math. In this guide, we delve into the financial complexities of this decision, using a concept known as the "Renting vs. Buying Breakeven Point" to provide a comprehensive analysis.

Unraveling the Costs of Home Ownership

Homeownership is often equated with financial stability and success. However, it comes with its own set of unrecoverable costs that can significantly impact your financial health. These costs can be broadly categorized into six components: property taxes, maintenance costs, homeowners association (HOA) fees, insurance, transaction costs, and the cost of capital.

Property Taxes

As a homeowner, you are required to pay property taxes to your local government. These taxes are typically calculated as a percentage of your home's value and can vary significantly depending on your location. For instance, if your home is valued at $1 million and the property tax rate in your area is 1.2%, you would pay $12,000 annually in property taxes.

You may think that these are costs you pay to fund the school district and such. However, if you were to rent a single family home in the same neighborhood you would still send your kids to the same school. This part of the argument isn’t valid.

Maintenance Costs

Owning a home also means being responsible for its upkeep. From minor repairs to major renovations, these costs can add up over time. A common rule of thumb is to budget 1% of your home's value each year for maintenance costs. For a $1 million home, this would equate to $10,000 per year.

To clarify, maintenance costs are the boring things that don’t add value to your home. These are items like when your washing machine breaks or your roof needs new shingles. Capital improvements such as a new addition or adding a pool can significantly change the value of your house and your tax assessment as well.

Homeowners Association (HOA) Fees

If you're considering a condo or a property within a planned community, you'll likely have to pay HOA fees. These fees cover the cost of maintaining common areas and providing shared amenities. In a city like New York, HOA fees can range from a few hundred to several thousand dollars per month and are usually based on the size of your apartment.

Insurance

Homeowners are typically required to have homeowners insurance, which covers potential damages to the property. The cost of this insurance can vary widely depending on factors like the home's value, location, and the specifics of the policy. On average, homeowners insurance costs around $1,200 per year, but this can be higher for more expensive homes or homes in areas prone to natural disasters. This type of insurance is required by your mortgage lender and is usually significantly more expensive than renters insurance.

Transaction Costs

Buying and selling a home involves significant transaction costs, including real estate agent commissions, closing costs, and moving expenses. These costs typically amount to 2-5% of the home's purchase price. For a $1 million home, this could equate to $20,000 to $50,000 each time you buy or sell. Some states such as New York have a “Mansion Tax” equal to 1% of your property value if your home is over $1M. There is also the “Mortgage Recording Tax” which can be 1-1.5% of your mortgage value. Both of these are due at closing. On a $1M NY property with $200,000 down, you are looking at $10,000 in Mansion Tax, and upwards of $12,000 in Recording taxes after the brokers fees and other paperwork.

Cost of Capital

This is perhaps the most complex and significant cost associated with homeownership. The cost of capital includes the interest you pay on your mortgage and the opportunity cost of investing your down payment in the property instead of other potentially lucrative investments. For example, if you take out a $800,000 mortgage with a 6.5% interest rate, your annual interest cost would be $52,000.

Decoding the Cost of Capital

The cost of capital is a critical factor in the rent vs buy decision. It comprises two main components: the opportunity cost of the down payment and the cost of the loan.

Opportunity Cost of the Down Payment

When you buy a home, you typically make a down payment. This money is now tied up in your home and can't be used for other investments. The potential returns you miss out on by not investing this money elsewhere is known as the opportunity cost. For instance, if you make a $200,000 down payment and could have earned a 7% return on that money in the stock market, your opportunity cost would be $14,000 per year.

Cost of the Loan

If you take out a mortgage to buy your home, you'll have to pay interest on the loan. This interest is a cost that you wouldn't have incurred if you had chosen to rent instead. For example, if you take out a $800,000 mortgage with a 6.5% interest rate, your annual interest cost would be $52,000.

The Renting vs Buying Breakeven Model

To make an informed decision between renting and buying, we can use the concept of a “Renting vs. Buying Breakeven Point" model. This concept aims to calculate the total unrecoverable costs of homeownership and compare them to the cost of renting. If the cost of renting is less than the breakeven point, renting may be the more financially sensible option.

Some Additional Factors and Considerations In Our Model

Loan Amortization

Over the life of your mortgage, the amount of your payment that goes towards interest decreases while the amount that goes towards the principal increases. This means that over time, you're building equity in your home faster. Your cost of loan will be highest in year 1 of your analysis and slowly decrease.

Mortgage Tax Deductions

One of the benefits of homeownership is the ability to deduct mortgage interest from your taxable income. This can provide significant tax savings, especially for high-end professionals in higher tax brackets. However, it's important to note that the tax benefits of homeownership have been reduced in recent years due to changes in tax laws.

Home Price Appreciation

Over the long term, home prices tend to increase. This appreciation can significantly impact your return on investment. For instance, if your home appreciates at an average rate of 3% per year, a $1 million home would be worth over $1.3 million in 10 years. Homes across the US generally appreciate in line with the rate of inflation, and while some hot markets have faster appreciation - we are going to take this out of our model for now.

Comparison to Stock Market Investments

While home price appreciation can provide a significant return, it's important to compare this to potential returns from stock market investments. Historically, the stock market has provided an average annual return of about 7%. This means that the opportunity cost of investing your down payment and the added monthly equity in your home could be significant. We are going to leave this opportunity cost out for now.

Bringing the Numbers to Life With A Model

To help illustrate these concepts, let's consider a hypothetical scenario. Suppose you're considering buying a home valued at $1 million. You plan to make a 20% down payment ($200,000) and take out a 30-year mortgage for the remaining $800,000 at an interest rate of 6.5%.

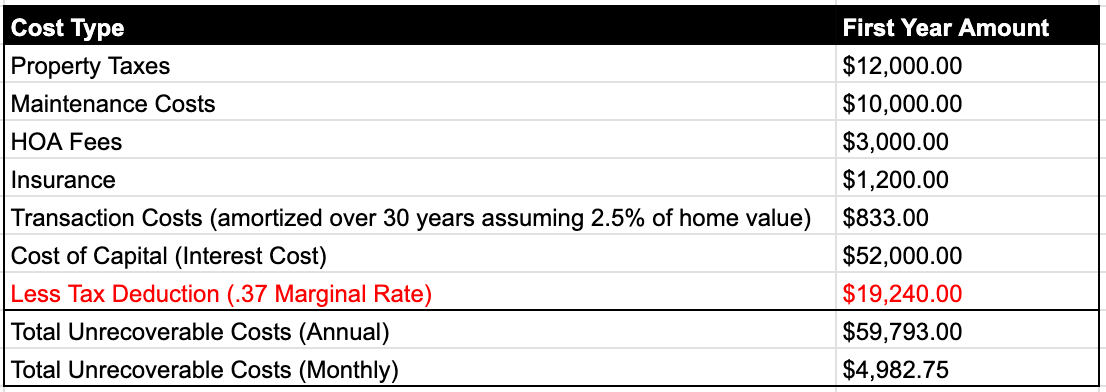

Here's a breakdown of the annual unrecoverable costs of homeownership:

This equates to $6,586 per month.

Now, let's consider the impact of loan amortization and mortgage tax deductions as adjustments:

Loan Amortization: Over the life of your mortgage, the amount of your payment that goes towards interest decreases while the amount that goes towards the principal increases. This means that over time, you're building equity in your home faster. In the first year of your mortgage, you would pay approximately $52,000 in interest. However, by the 30th year, your annual interest payment would decrease to around $2,000.

Mortgage Tax Deductions: In the United States, homeowners can deduct mortgage interest from their taxable income. This can provide significant tax savings. For instance, if you're in the 37% tax bracket and you pay $52,000 in mortgage interest in the first year, this deduction could save you about $19,240 on your tax bill.

To incorporate these factors into our model, we can adjust the cost of capital to account for the tax savings from the mortgage interest deduction. This would reduce the cost of capital in the first year from $52,000 to $32,760 ($52,000 - $19,240).

So, the adjusted annual unrecoverable costs of homeownership in the first year would be $59,793 (property taxes of $12,000, maintenance costs of $10,000, HOA fees of $3,000, insurance of $1,200, transaction costs of $833, and adjusted cost of capital of $32,760), or $5,014 per month.

If you can rent a similar home for less than this amount, the breakeven point suggests that renting would be the more financially sensible option in the first year. However, as the interest portion of your mortgage payment decreases over time, the tax savings from the mortgage interest deduction will also decrease. This means that the breakeven point will increase over time.

As you can see, this model is also highly sensitive to interest rate adjustments. If you were lucky enough to finance this mortgage in 2022 with a 2.5% APR, your annual Cost of Capital would drop to $20,000 and your Monthly breakeven point drops to a staggeringly low $3,302.75. This is why it’s often a good idea to invest in properties right after a disaster when the Fed tries to stimulate the economy. If you move fast enough you can score a great mortgage before home prices appreciate significantly.

Beyond the Numbers: Other Considerations in the Renting vs Buying Decision

While the financial aspect is a crucial part of the rent vs buy decision, it's not the only factor to consider. There are several non-financial benefits and drawbacks to both renting and buying that can significantly impact your decision.

Flexibility

Renting offers a level of flexibility that homeownership can't match. As a renter, you're not tied down to a property for the long term. If your circumstances change - for example, if you get a job offer in a different city - you can move without the hassle of selling a property.

Control and Stability

On the other hand, owning a home gives you a level of control and stability that renting can't provide. You have the freedom to modify your home to suit your tastes, and you don't have to worry about rent increases or eviction.

Building Equity

One of the significant advantages of homeownership is the ability to build equity. As you pay off your mortgage, you're gradually increasing your ownership stake in the property, which can be a powerful wealth-building tool.

Saving A Down Payment

It’s no easy feat putting together a significant downpayment for a home. Most people handle these in a more conservative savings account rather than putting these into the market to avoid any potential market volatility. While you protect your downside risk this way, you also limit the upside of a bull run. I wrote another article about where to keep your house downpayment savings recently.

The Final Word: Navigating Your Path

The decision to rent or buy is a significant one, with far-reaching financial and lifestyle implications. By understanding the costs associated with each option and considering your personal circumstances and goals, you can make an informed decision that aligns with your financial strategy and lifestyle preferences.

Remember, the Renting vs. Buying Breakeven Point is a tool to guide your decision-making process, not a definitive answer. It provides a starting point for your analysis, but your final decision should take into account all the factors we've discussed, from the financial costs to the non-financial benefits and drawbacks. Worst case scenario, this can help you anchor your financial argument with a more emotionally driven spouse.

Whether you choose to rent or buy, the most important thing is to make a decision that supports your financial health and lifestyle goals. After all, a home is more than just a financial investment - it's a place to live, grow, and create memories.